In case you haven’t heard, Uber, the 4 year-old technology and transportation startup, raised a whopping $1.2 billion in funding from mutual fund managers and venture capitalists last month. This financing round placed Uber’s valuation at approximately $17 billion.

If you’re not familiar with Uber and what they do, just imagine a black-car or taxi service you can request via iPhone or Android app. You open the app, the app tracks your current location, you tap “Request an Uber”, and minutes later a driver picks you up. At the end of the trip, you pay through the app, with the credit card you’ve signed up with.

But the question remains, is the valuation reasonable or are the investors crazy? The short answer: yes, it’s quite reasonable. The long answer: not only is it reasonable, it’s actually undervalued!

An article on Business Insider states that an anonymous investor (not an investor in Uber) heard that Uber’s gross revenue last year (2013) was $750 million with $150 million in cash flow. He continues on to say that Uber’s projected cash flow for 2014 is around $400 million.

Doing a quick and crude calculation will show that Uber is being valued at a multiple of 23x gross revenue ($17 billion / $750 million). According to this data set provided by NYU Stern, the Internet Software and Services industry’s typical EBIT multiple is 33.63x. Obviously, this comparison is not exact, but it puts things into perspective. Uber can certainly fall within other industries but their main selling point is their software, so I chose to compare it to the software sector. Based solely on this analysis, it seems that Uber’s multiple is actually acceptable.

However, in the world of startups and venture capitalists, traditional valuation multiple formulas rarely apply. Viewing the valuation from the lens of an investor, this deal might actually even be a huge bargain. For instance, Facebook back in 2007 raised money at a 100x multiple with only $153 million in revenue and a $138 million net loss according to Statista. With that in mind, Uber’s 23x multiple seems very reasonable.

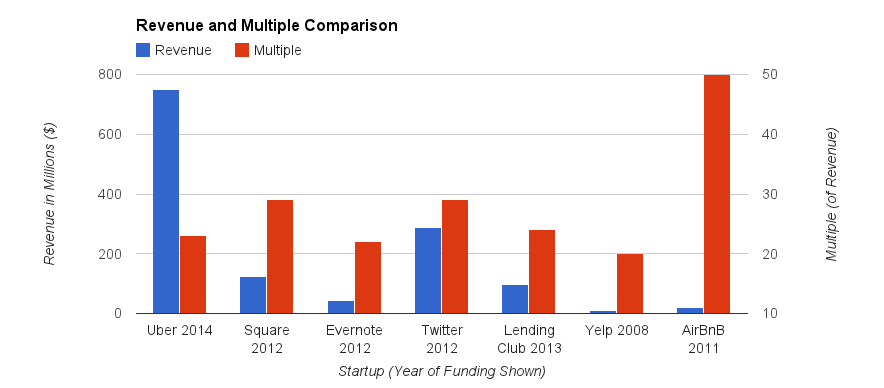

To illustrate this fact, I’ve created a chart below that compares companies’ revenues and their multiples for one of their funding rounds. I used Uber’s estimated 2013 gross revenue of $750 million and its $17 billion valuation to determine its multiple of 23x gross revenue below. I also plotted the revenue and multiple numbers for other superstar startups on the chart. I tried to choose funding rounds that resulted in a multiple within the range of Uber’s 23x revenue. I’ve also included one extreme example, AirBnb, just to represent the other end of the spectrum.

Comparing Uber’s revenue and multiple to the other startups, it’s easy to see that its valuation isn’t as crazy as it seems. Other startups had multiples that were much higher relative to their revenue at the time of funding. Amongst its peers, Uber is definitely looking like a winner.

To further support Uber’s valuation, a report from IBISWorld estimates that the 2014 annual profit for the Taxi & Limousine industry will be $1.4 billion. Essentially, Uber is projected to make approximately 29% of what the entire Taxi industry is expected to make!

With Uber’s “alarming” growth rate and new infusion of cold hard cash, you can bet that the company is dead set on conquering this exciting industry where transportation meets technology. There’s no doubt in my mind that the $17 billion valuation is justified. As a matter of fact, it’s definitely too low.

Sources:

Statista, IBISWorld, NYU Stern, Business Insider, CNN